Avoid Killing Your BaaS Programme: Why the open-switch model wins

A BaaS (Banking as a service) program built on a closed middleware network is a program designed to fail. This model sacrifices control, introduces compliance risks, and creates a dependency that results in high costs and low partner stickiness.

Conversely, the open-architecture "switch" model is the strategic choice for an enduring BaaS program. This approach prioritizes direct relationships, leverages open protocols, and ensures full control and compliance - the foundational pillars of a scalable and successful embedded finance future.

This article dissects the two primary BaaS models, a closed middleware network versus an open architecture switch and explains why this choice is the most pivotal strategic decision your institution will make.

The two BaaS models

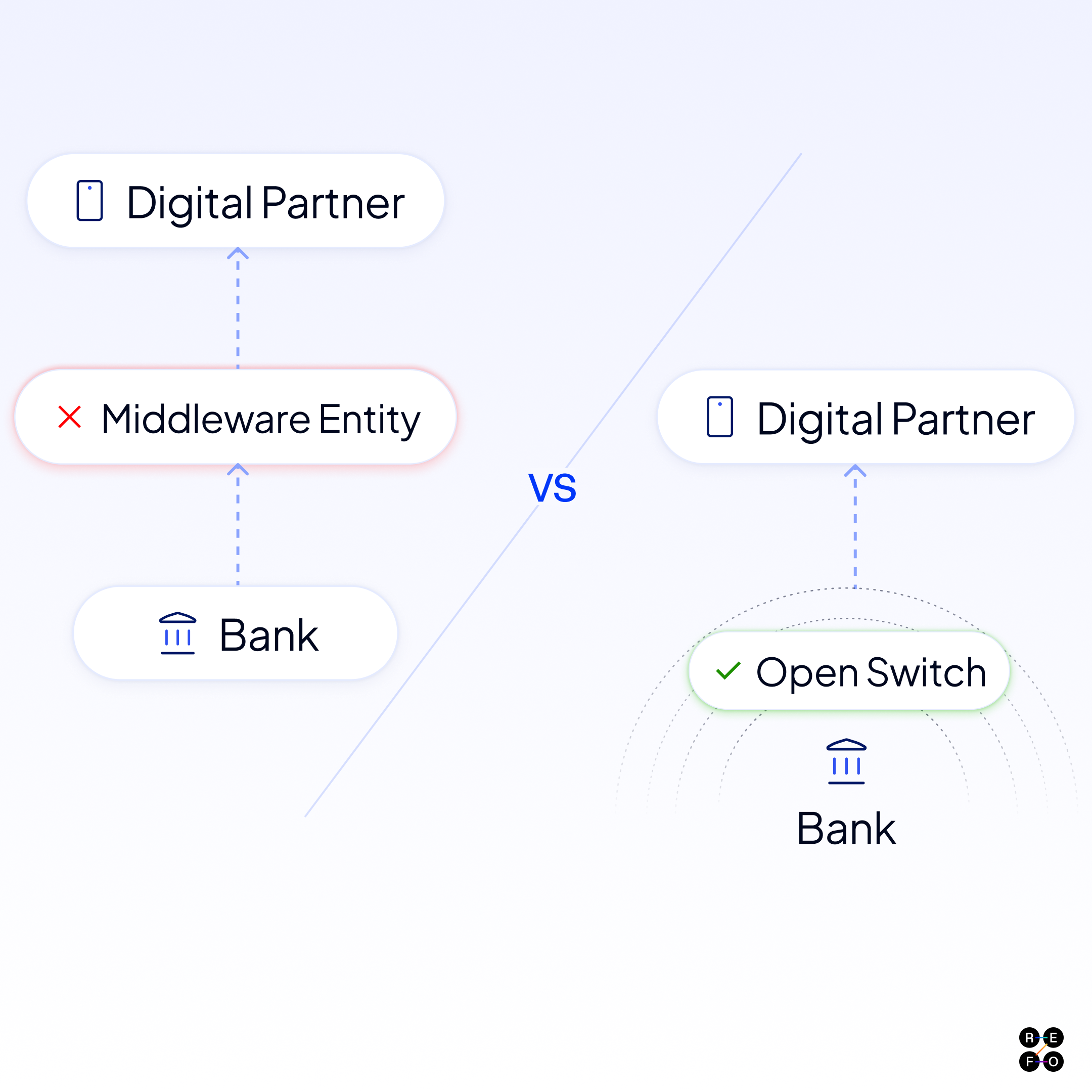

Model 1: Closed middleware network

This model introduces a third-party, proprietary middleware provider as a central hub between a bank (FI) and its partners. The middleware promises a single integration point to a broad network, but it creates a three-entity ecosystem: the bank, the middleware, and the digital partner.

Model 2: Open architecture "Switch"

This model eliminates the third-party intermediary. The technology stack, which functions as a switch, sits directly on the bank's side and connects the bank directly to digital partners through an open network. This creates a direct, two-entity ecosystem between the bank and the partner, with the switch acting as a direct conduit, not an intermediary.

A head-to-head comparison

A strong regulatory ask

In the U.S., recent consent orders have made clear that banks must demonstrate direct control, risk assessments, and exit planning for fintech partnerships.

In India, the RBI’s digital lending guidelines, IT outsourcing framework, and enforcement actions point in the same direction banks must avoid dependency on opaque intermediaries and ensure operational resilience.

An open switch architecture satisfies these global supervisory expectations by keeping integration, governance, and resilience directly under the bank’s control.

Open switch should be your next architecture

The race to build a successful Banking-as-a-Service (BaaS) program is on, but a critical architectural misstep can kill the initiative before it starts. We strongly recommend Model 2 : Open switch architecture as the preffered model.

Refo operates on an open-architecture model that provides the technology to power a bank's embedded banking journey directly on the FI's side. By adhering to open protocols, this model ensures that the bank retains full control and avoids the vendor lock-in common with closed proprietary systems.

At Refo, we work closely with global banks to define and accelerate their BaaS programmes. Want to explore how we can help you? Contact us today.